Clarifying the 2013 Capital Gains Rates

Clarifying the 2013 Capital Gains RatesIt has been universally reported that under the newly passed American Taxpayer Relief Act of 2012, net capital gain tax rates have risen to 20% for taxpayers with taxable income greater than $400,000 for single filers and $450,000 for joint filers. To clarify this broad statement, under IRC §102 of the new law, the higher capital gains rate applies only to the gain that, when added to other taxable income, exceeds the threshold amounts. Taxpayers below the 39.6% taxable income threshold before capital gains are taken into account will have their capital gains taxed at 15% up to the taxable income threshold and 20% on the excess. The following two examples illustrate how the net capital gain tax rate is calculated:

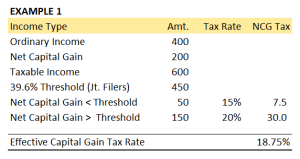

In Example 1, joint taxpayers earn $400,000 of ordinary income and another $200,000 in net capital gains. Under the new law, the first $50,000 of net capital gains is taxed at the lower rate, with the remaining $150,000 taxed at the higher rate. The effective rate of 18.75% reflects the blending of the 15% and 20% rates.

courtesy: Posted January 2, 2013 by Phil Karter, TaxBlawg.net

***

| 2013 Federal Capital Gain Tax Rates | |||||||||||||||||||||||||

|

Starting in 2013, the tax rate on long-term capital gains will be 20% for filers making income over $400K(single)/$450K (MfJ). Starting in 2013, the distinction between ordinary and qualified dividends will disappear, and all dividends will be subject to the ordinary tax rates.

• 20 PERCENT CAPITAL GAIN TAX IN 2013

The Tax Relief, Unemployment Insurance Reauthorization and Jobs Creation Act of 2010 extends the Bush-era tax cuts until the end of 2012. Beginning January 1, 2013, the tax rate will revert from the current 15% rate back to the former 20% capital gain tax rate that was in effect prior to 2003.

Beginning in 2013, capital gain income will be subject to an additional 3.8% Medicare tax. The net effect of both capital gain tax increases is a new 23.8 percent tax rate for higher earners—the highest rate for long-term capital gains since 1997. The Joint Committee on Taxation estimates the new Medicare tax on investments will cost taxpayers over $30 billion annually.

Beginning in 2013, capital gain income will be subject to an additional 3.8% Medicare tax. The net effect of both capital gain tax increases is a new 23.8 percent tax rate for higher earners—the highest rate for long-term capital gains since 1997. The Joint Committee on Taxation estimates the new Medicare tax on investments will cost taxpayers over $30 billion annually.

Higher-income taxpayers could see the capital gains tax go from the existing 15% to 23.8% in 2013. Top investment earners next year could face a 43.4% tax on dividends: 39.6% maximum income tax rate plus the 3.8% health care surtax.

Reference: foxbusiness.com

No comments:

Post a Comment